Buying your first home can seem daunting even at the best of times.

Add in the uncertainty brought on by the pandemic and getting into the real estate market for the first time can feel even more unnerving.

The good news is that with the right advice and some preparation, your dream of homeownership can become a reality.

For those considering taking the leap and buying their first home, here are the answers to five common questions answered by a TD mortgage specialist to help determine your readiness, along with what you need to know to make an informed decision.

Is now a good time for me?

There's a lot of change happening in the world of real estate today. Canadian mortgage rates are hovering new historic lows, opening the door for many would-be first-time buyers.

On the other hand, the Canadian Mortgage and Housing Corporation (CMHC) has recently made a number of policy changes including increasing credit score demands, and limiting down payment sources for those needing default insurance from CMHC for buyers who have paid less than 20 per cent as a down payment on a home.

And while it's always a good time to start learning about and planning for homeownership, with so many changes afoot, it's a good idea to get the latest information by reaching out to a mortgage specialist who can help lay out your next steps towards the path to first-time home ownership, according to Mike French, Senior Vice President of Real Estate Secured Lending at TD.

"It’s wise to seek the advice of a mortgage specialist or financial advisor so you understand how to budget for all these variables," French said.

"Not only can they help you determine what you need, but they can also be a source of support if you run into any unforeseen difficulties during the buying process."

What incentives are available to me as a first-time home buyer?

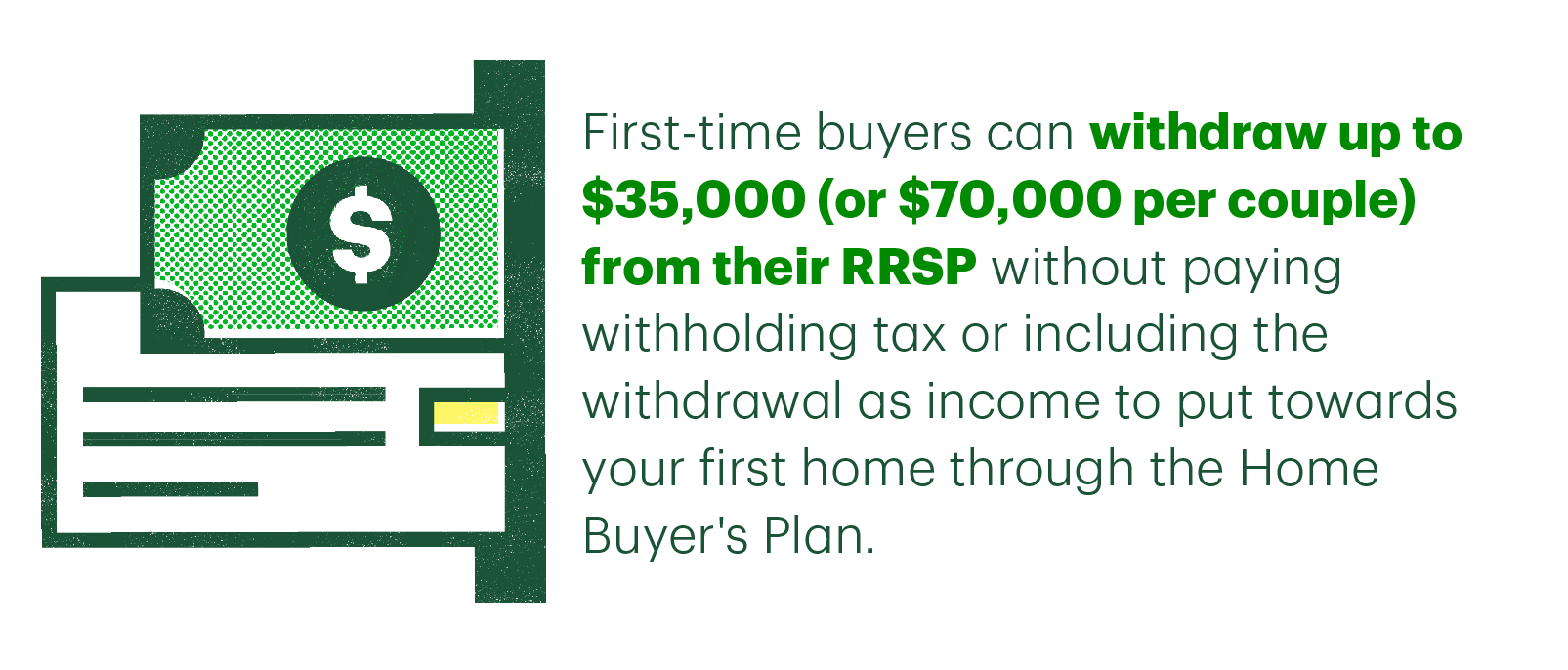

First-time buyers can withdraw up to $35,000 (or $70,000 per couple) from their RRSP without paying withholding tax or including the withdrawal as income to put towards your first home through the Home Buyer's Plan. Repayments begin two years after you withdraw the funds, and you have fifteen years to completely repay your RRSP. To see if you meet the Canada Revenue Agency’s (CRA) eligibility criteria and other conditions, review the information here.

What is the first thing I should do to make sure I'm financially prepared to own a home?

"Before you start planning open house visits or virtual tours, it's crucial to understand what you can afford by assessing how your lifestyle and other financial obligations will affect the size of your mortgage, while ensuring you can comfortably afford mortgage payments should interest rates rise in the future," French said.

"Take a look at your broader financial picture and assess your financial readiness, such as: how much do you have for a down payment; how would a new home impact your cash flow; do you have any debt or other financial considerations; do you have any money set aside for an unexpected cost that could arise associated with a new home."

The TD Mortgage Affordability Calculator can help you determine a potential price range for your first home and help you understand how much mortgage may be comfortable for you after taking into consideration how much you've saved for a down payment, your monthly expenses, savings, and how much debt you might have.

Should I test drive my mortgage payments before buying?

"Test drives aren't just for buying cars," French said.

"As you get closer to buying a home, consider taking your monthly mortgage payments for a test-drive by making an automatic transfer of the difference in amounts between your anticipated mortgage amount and your current housing costs into a TFSA or high-interest savings account for a few months," French said.

"This approach allows you to see how comfortably you can manage the monthly mortgage amount, while also helping you save for a larger down payment."

Create a monthly budget that includes all expenses you would take on as a homeowner and see how it impacts your lifestyle over a three to six-month test period. This way, you will know what you are and aren't willing or able to sacrifice for your new home and adjust your price range, if needed.

What are some of the 'hidden' costs I should plan for?

Ongoing payments, (for example, mortgage payments, property taxes, maintenance and utilities) and one-time expenses, (including property assessments and surveys; home inspection fees; land transfer taxes; notary, legal and title insurance fees; property tax and utility adjustments and moving costs) are not the only costs to plan for as a homeowner.

'Hidden' or 'unexpected' costs can have a big impact on your ability to afford your mortgage payments down the road, and you don't want to be caught off guard. Costs in this category include interest rate increases, unforeseen repairs, changes to the stability or status of your income, and even pest control, landscaping and renovation expenses.

"It's always important to build a buffer into your total budget so you can be prepared for unexpected costs," French said.

"Plan ahead and ensure you have an emergency fund set up that can cover your living expenses including your housing costs, so you are able to stay afloat should something happen and you find yourself unable to work."

The Financial Consumer Agency of Canada recommends having the equivalent of three to six months of expenses or income in your emergency fund.

TD offers Mortgage Critical Illness Insurance and Life Insurance that can help reduce or paydown an outstanding TD Mortgage balance in the event that you were to suffer a health event that is covered by your policy.1

Learn more about home ownership and how to find the right mortgage for you on our First-time Homebuyer's page.

1. Accidental dismemberment coverage underwritten by TD Life Insurance Company. All other coverages underwritten by The Canada Life Assurance Company. TD Life Insurance Company is the authorized administrator for this insurance. For more details on insurer and/or administrator, as well as all benefits, limitations and exclusions, please refer to the Certificate of Insurance.

Want to learn more about your money?